"...When evaluating a problem of such magnitude, one might as well begin with the problem as the Europeans see it — namely, that their banks’ biggest problem is rooted in their sovereign debt exposure.

The state-bank contagion problem is fairly straightforward within national borders. As a rule the largest purchaser of the debt of any particular European government will be banks located in the particular country. If a government goes bankrupt or is forced to partially default on its debt, its failure will trigger the failure of most of its banks. Greece does indeed provide a useful example.

Until Greece joined the European Union in 1981, state-controlled institutions dominated its banking sector. These institutions’ primary reason for being was to support government financing, regardless of whether there was a political or economic rationale justifying that financing. The Greeks, however, have no monopoly on the practice of leaning on the banking sector to support state spending. In fact, this practice is the norm across Europe.

Spain’s regional banks, the cajas, have become infamous for serving as slush funds for regional governments, regardless of the government in question’s political affiliation. Were the cajas assets held to U.S. standards of what qualifies as a good or bad loan, half the cajas would be closed immediately and another third would be placed in receivership. Italian banks hold half of Italy’s 1.9 trillion euros in outstanding state debt. And lest anyone attempt to lay all the blame on Southern Europe, French and Belgian municipalities as well as the Belgian national government regularly used the aforementioned Dexia in a somewhat similar manner.

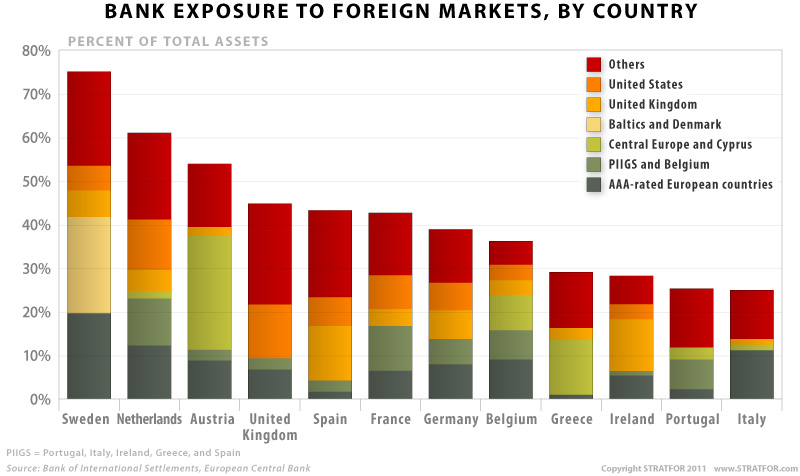

Yet much debt remains for outsiders to own, so when states crack, the damage will not be held internally. Half or more of the debt of Greece, Ireland, Portugal, Italy and Belgium is in foreign hands, but like everything else in Europe the exposure is not balanced evenly — and this time, it is Northern Europe, not Southern Europe, that is exposed. French banks are more exposed than any other national sector, holding an amount equivalent to 8.5 percent of French gross domestic product (GDP) in the debt of the most financially distressed states (Greece, Ireland, Portugal, Italy, Belgium and Spain). Belgium comes in second with an exposure of roughly 5.5 percent of GDP, although that number excludes the roughly 45 percent of GDP Belgium’s banks hold in Belgian state debt..."

at http://www.marketoracle.co.uk/Article31125.html

The state-bank contagion problem is fairly straightforward within national borders. As a rule the largest purchaser of the debt of any particular European government will be banks located in the particular country. If a government goes bankrupt or is forced to partially default on its debt, its failure will trigger the failure of most of its banks. Greece does indeed provide a useful example.

Until Greece joined the European Union in 1981, state-controlled institutions dominated its banking sector. These institutions’ primary reason for being was to support government financing, regardless of whether there was a political or economic rationale justifying that financing. The Greeks, however, have no monopoly on the practice of leaning on the banking sector to support state spending. In fact, this practice is the norm across Europe.

Spain’s regional banks, the cajas, have become infamous for serving as slush funds for regional governments, regardless of the government in question’s political affiliation. Were the cajas assets held to U.S. standards of what qualifies as a good or bad loan, half the cajas would be closed immediately and another third would be placed in receivership. Italian banks hold half of Italy’s 1.9 trillion euros in outstanding state debt. And lest anyone attempt to lay all the blame on Southern Europe, French and Belgian municipalities as well as the Belgian national government regularly used the aforementioned Dexia in a somewhat similar manner.

Yet much debt remains for outsiders to own, so when states crack, the damage will not be held internally. Half or more of the debt of Greece, Ireland, Portugal, Italy and Belgium is in foreign hands, but like everything else in Europe the exposure is not balanced evenly — and this time, it is Northern Europe, not Southern Europe, that is exposed. French banks are more exposed than any other national sector, holding an amount equivalent to 8.5 percent of French gross domestic product (GDP) in the debt of the most financially distressed states (Greece, Ireland, Portugal, Italy, Belgium and Spain). Belgium comes in second with an exposure of roughly 5.5 percent of GDP, although that number excludes the roughly 45 percent of GDP Belgium’s banks hold in Belgian state debt..."

at http://www.marketoracle.co.uk/Article31125.html